Auctus Metals Client Portfolios Breaks +54% Annual Net Returns For Year 2019

Posted on 15 Jan, 2020 in

Auctus Metals Client Portfolios Breaks +54% Annual Net Returns For Year 2019

We Are Facing A Spectacular Perfect Storm In Precious Metals

But Especially In Platinum Group Metals

13 Jan 2020

Auctus Metals Portfolio Management of Physical Metals

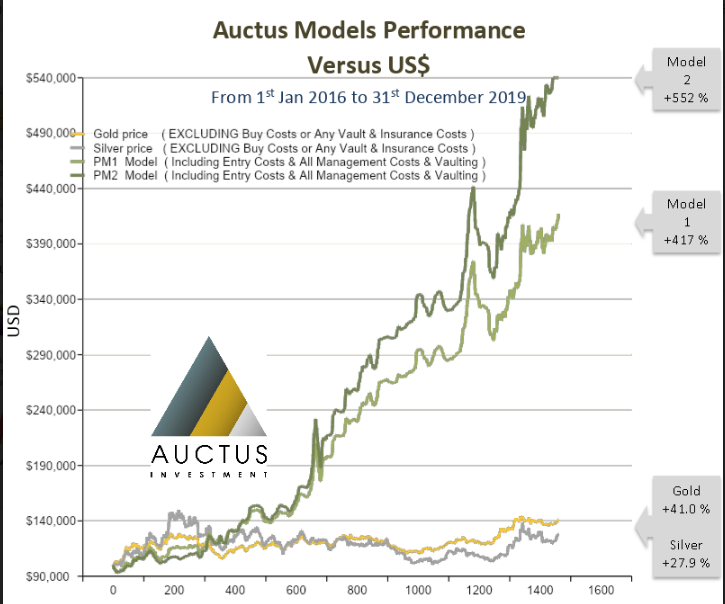

Report on our performances in 2019 and since Year 2016 is attached

Our 2019 performance has yet again proven our portfolio management offering far outstripping the market. All supported by physical holdings in our own client’s vaults.

These models are designed to give a very healthy positive (+Alpha) return over a 3 to 4 year period ‘over and above gold’s performance’. Although saying that we have walked into the perfect storm (which we have written about here) and we do expect returns on our models to stay elevated over the next few years.

Recent Market News

Platinum Group Metals – South Africa

South Africa is the world’s leading producer of platinum group metals (PGM’s) by value and volume. In 2018, it accounted for 73 percent of the world’s platinum mine production, 39 percent of the world’s palladium production, and 82 percent of the world’s rhodium production.

South Africa’s mine production of PGM’s come from extremely deep mine shaft systems of several miles deep, six of the ten deepest mines in the world reside in a particular region of South Africa. These mine shafts at their most deep depths are superheated from replenishing magma, hence the classification as magma mines. The mineshafts demand huge amounts of machinery infrastructure and a 100% consistent electricity supply. They are now directly affected by the energy crisis in South Africa, with regular mineshaft closures now commonplace.

2nd January Update : CAPE TOWN – As 2020 dawns in South Africa, energy experts are warning that load shedding (major energy cuts) will be with us for another five years at least for the country as a whole. Read here.

South Africa’s electricity utility, Eskom, announced unprecedented Stage 6 load-shedding last week. The company cut 6,000 MW from the national grid, which is around 20% of the country’s demand. Eskom provides 95% of South Africa’s electricity, but plant maintenance and unplanned breakdowns meant the company was operating at just 55% capacity.

South African PGM supply was reduced by 50% as producers suspended operations. South African 5E PGM (platinum, palladium, rhodium, ruthenium, and iridium) mining capacity fell by almost a half in December after the escalation to Stage 6 load-shedding led to a one-day suspension of underground mining shifts. While load-shedding is not uncommon, it is the first time since 2008 that it has led to mine stoppages. However, a backlog of existing

concentrate stocks will minimise refined output losses for the year 2019, moving forward is a different picture.

Eskom is now a greater risk to South African PGM supply going forward. Eskom had previously considered Stage 4 the most extreme level of load-shedding; this is the first time in history that Stage 6 has been implemented. The escalation to Stage 6 represents a new level of threat to the industry.

Global Economic Backdrop

Precious Metals Price Prognosis Moving Forward

National governments have found a new impetus for increased deficit spending even in the face of our global debt crisis, ignoring problems rarely solves them. You need to deal with them and not just the effects, but the underlying causes, or else they usually get worse – a lot worse.

As a quick bullet point overview of just some of the economic, macro and political conditions that will drive the gold and precious metal prices in 2020 and beyond. Investors and more importantly everyone should now be extremely aware of what is developing very quickly at this point …..

- The turn of the credit cycle is now with us. The effect on government deficits and how they are going to be financed is now front and centre. Deficits can only be financed by monetary inflation and all governments globally are expanding their deficit spending rapidly. USA Federal spending increased by over +7% in the previous 12 months, while growth was just 3% (is deficit spending giving a massively false impression of real growth, I would suggest without a doubt it is !).

- MMT – globally the political and monetary authorities are embracing ‘Modern Monetary Theory’ as the only way forward for them, which is extreme debt monetization (severe currency value destruction).

- Re-emergence of currency debasement, USA Fed began aggressively injecting new money into a shockingly illiquid banking system through repurchase agreements as US$ repo interest rates soared up to 10%, ECB has also re-started Quantitative Easing in November, while China looks for ways of bailing out its shadow banking sector through a massive expansion of the monetary base (to read more about this please look for articles relating to the REPO crisis).

- Global Economy slides into recession, considering this has been the longest economic expansion in history at 127 months and counting as of January 2020 in the USA, and the fact freight volumes globally have collapsed, Baltic Dry Index off -39% since September points to a dangerous picture ahead (average expansion in USA is 38.7 months between years 1854 to 2009, longest ever previous expansion was March 1991 to March 2001 at 120 months).which we will have to deal with painfully in the not-too-distant future. This wasn’t a “beautiful deleveraging” as they initially referred; it is the ugly creation of bubbles and misallocation of capital. Central banks have now lost control of the global monetary system.

- The European banking system is completely illiquid, Deutsche bank, Commercz bank and Unicredit bank for examples are considered potentially insolvent institutions, kept on life support by the ECB and central banks. This is a full crisis coming that is unavoidable.

- As interest rates spike higher over this credit cycle in the face of the liquidity debt crisis the last housing bubbles globally will collapse, further compounding the negative macro-economic picture.

- Stock markets have been solely driven by largesse capital injections and lower interest rates from the central banks, Case Shiller PE ratio of the S&P500 is now trading at levels last seen in 1930 and year 2000 (both ended very badly), I am not saying stock markets are about to collapse, but an awareness of real value versus bubble territory must be understood.

- War Footings: Political and religious crisis in the Middle East continues to intensify. The strike against one of Iran’s most prominent top generals Soleimani will not go unanswered. The Iranian leadership does not want to appear weak and will pick their retaliation and timing of their escalation, and will most likely be very harmful, much higher oil prices?

- Global mine production falls in silver, gold and platinum group metals will continue over the next few years, driven by falling ore grades, higher energy prices (escalation in the Middle East will only compound this), the cost of production rises pushing further mine and pit closures due to loss-making enterprises etc.. All of this further escalating the supply/demand deficit constraints now being recorded globally.

The year 2020 and beyond is shaping up to be the year that all semblance and consideration for paper money’s role as a store of value is abandoned. 2020 onwards could well be the recognised period when currencies begin to be visibly shattered in the hands of their long-suffering users and holders.

Please contact our specialist team at Goldstackers to discuss how you can protect your portfolio by adding precious metals to your portfolio.